Home

HomeGlobal Robot Installations Top 500,000, Yet Partner Ecosystem Remains Complex

# europe

# asia

# abb robotics

# FANUC News

# Integration

# kuka robotics

# systems integrator

# Universal Robots

# yaskawa

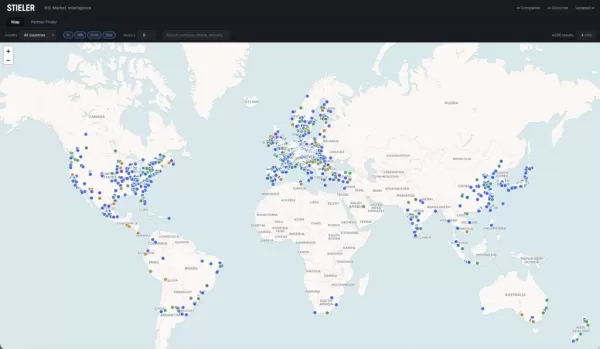

A recent global study has analyzed the dynamics between robot manufacturers and system integrators. Click to enlarge. Source: STIELER Technology & Market Advisors, RSI Market Intelligence

The true bottleneck: Even the world's most sophisticated AI-powered robot cannot deploy itself. The notion that collaborative robots would render system integrators obsolete has been debunked.

Even relatively simple robots demand specialized application knowledge, integration of peripheral equipment, thorough risk assessments, and process-specific expertise. The system integrator is not merely an add-on service but the critical enabler. Without their involvement, even superior technology remains idle on the display floor.

A database reveals the ecosystem

Over half a million industrial robots are installed globally each year. Yet the ecosystem responsible for their deployment—comprising system integrators, machine builders, and distributors that transform hardware into functional applications—remains poorly documented. There is no unified, international overview detailing these companies' identities, specializations, operational regions, or competitive standings.

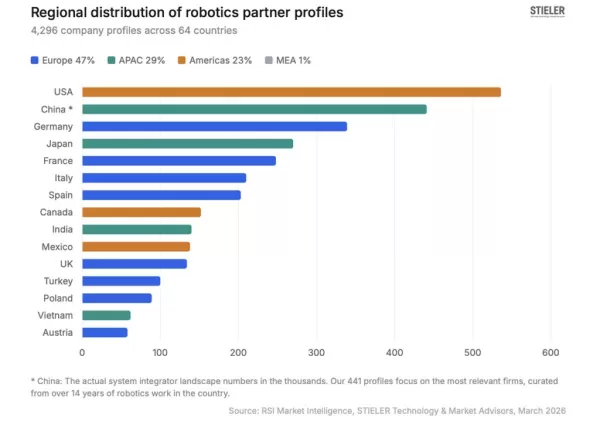

For the past year, we have worked to create such an overview. The outcome is a structured database containing 4,296 company profiles across 64 countries. Below are some of the key trends identified.

This analysis relies on a structured dataset compiled from OEM partner directories, corporate websites, business registries, industry associations, screenings of major trade-show exhibitors, and analyst reviews. While coverage differs by country and online visibility, the structural trends are evident.

A vast ecosystem led by small enterprises

Among the approximately 3,400 companies with available employee data, 54% have fewer than 50 staff members. Only 5% employ over 1,000 people. The top 5% of firms by headcount represent 84% of total employment in the dataset—a classic long-tail distribution. The robotics ecosystem consists of a handful of large conglomerates and numerous specialized small firms.

Regionally, Europe accounts for 47% of all profiles, APAC for 29%, and the Americas for 23%. The top five countries—the United States (536), China (441), Germany (339), Japan (270), and France (248)—comprise 43% of the total.

China presents a unique scenario. The actual number of system integrators likely reaches into the thousands, but many smaller entities lack a web presence, and the market is rapidly consolidating. Our 441 Chinese profiles are drawn from over 14 years of project work in the country—the actual ecosystem is far more extensive than any structured database can fully represent.

A significant portion of the channel operates independently

Related article

ABB Robotics Unveils OmniVance Autonomous Surface Finishing Cell

ABB Robotics stated that this finishing cell aims to bridge the gap between custom automation and entry-level toolkits. | Source: ABB RoboticsABB Robotics recently introduced its first fully automated sanding and polishing cell. The Zurich-based comp

FANUC America Announces $90 Million Investment in U.S. Robotics Manufacturing

FANUC is constructing a new facility to boost its robot manufacturing capacity in the United States. Source: FANUC AmericaAlthough the U.S. is a key robotics market, none of the top industrial automation companies are based there. This landscape is c

AI Robotics Transitions from Lab to Factory Floor

From left: Andy Lonsberry of Path Robotics; Anders Beck of Universal Robots; and Dave Coleman of PickNik Robotics.Artificial intelligence is now a fundamental part of every robotic system. It transforms how robots interpret sensor data, make decision

Related Special Topic Recommendations

Business

ABB Robotics Unveils OmniVance Autonomous Surface Finishing Cell

ABB Robotics stated that this finishing cell aims to bridge the gap between custom automation and entry-level toolkits. | Source: ABB RoboticsABB Robotics recently introduced its first fully automated sanding and polishing cell. The Zurich-based comp

FANUC America Announces $90 Million Investment in U.S. Robotics Manufacturing

FANUC is constructing a new facility to boost its robot manufacturing capacity in the United States. Source: FANUC AmericaAlthough the U.S. is a key robotics market, none of the top industrial automation companies are based there. This landscape is c

AI Robotics Transitions from Lab to Factory Floor

From left: Andy Lonsberry of Path Robotics; Anders Beck of Universal Robots; and Dave Coleman of PickNik Robotics.Artificial intelligence is now a fundamental part of every robotic system. It transforms how robots interpret sensor data, make decision

Related Special Topic Recommendations

Business

Best AI Expense Trackers: Scan Receipts & Categorize Corporate Spend Automatically

Best AI Expense Trackers: Scan Receipts & Categorize Corporate Spend Automatically

2026 Latest Best AI Expense Trackers: Top-rated tools to scan receipts & categorize corporate spend automatically. Discover powerful, game-changing solutions for effortless expense management, accurate financial tracking, and streamlined compliance. Our curated, weekly-updated comparison of free vs paid options helps you find the perfect fit. Unlock your AI edge with XIX.AI's expert picks.

10 tools

10 tools

xix.ai

Business

Best AI Recruiting Tools: Screen Resumes & Automate Candidate Interview Scheduling

xix.ai

Business

Best AI Recruiting Tools: Screen Resumes & Automate Candidate Interview Scheduling

Discover the 2026 latest top-rated AI recruiting tools on XIX.AI. Our curated list features powerful, game-changing solutions for screening resumes and automating candidate interview scheduling. Compare free vs paid options with real-world tests and weekly updated rankings. Find your perfect hiring assistant and streamline your recruitment today!

10 tools

xix.ai

Productivity

AI Personal Wellness & Focus Coaches: Manage Burnout & Boost Mental Energy Levels

Discover the 2026 best AI personal wellness and focus coaches on XIX.AI. Our curated rankings feature top-rated, game-changing tools to manage burnout and boost mental energy. Compare free vs paid options with real-world insights. Unlock your path to peak productivity and well-being today.

10 tools

xix.ai

chatbot

Top-Rated AI Romantic Chatbots: Build Long-Term Relationships with Consistent Personalities

Discover the 2026 latest top-rated AI romantic chatbots for building genuine, long-term connections. Our curated list features powerful, consistent personalities, free vs paid comparisons, and real-world tests. Find your perfect companion and start building today at XIX.AI.

10 tools

xix.ai

Education and Learning

Best AI Data Science Mentors: Master SQL, Pandas & Machine Learning Workflows

Discover the 2026 best AI data science mentors to master SQL, Pandas & ML workflows. Explore our top-rated, curated selection at XIX.AI for powerful, game-changing guidance. Compare free vs paid options with real-world insights. Unlock your data science mastery today.

10 tools

xix.ai

chatbot

Best AI Flirting & Conversation Trainers: Improve Social Charisma and Confidence in Real-Time

Discover the 2026 best AI flirting and conversation trainers on XIX.AI. Our curated, top-rated selection helps you build social charisma and confidence in real-time. Explore must-try, game-changing tools with free vs paid comparisons and weekly updated rankings. Unlock your social edge today.

10 tools

xix.ai

Comments (0)

0/500

Comments (0)

0/500

A recent global study has analyzed the dynamics between robot manufacturers and system integrators. Click to enlarge. Source: STIELER Technology & Market Advisors, RSI Market Intelligence

The true bottleneck: Even the world's most sophisticated AI-powered robot cannot deploy itself. The notion that collaborative robots would render system integrators obsolete has been debunked.

Even relatively simple robots demand specialized application knowledge, integration of peripheral equipment, thorough risk assessments, and process-specific expertise. The system integrator is not merely an add-on service but the critical enabler. Without their involvement, even superior technology remains idle on the display floor.

A database reveals the ecosystem

Over half a million industrial robots are installed globally each year. Yet the ecosystem responsible for their deployment—comprising system integrators, machine builders, and distributors that transform hardware into functional applications—remains poorly documented. There is no unified, international overview detailing these companies' identities, specializations, operational regions, or competitive standings.

For the past year, we have worked to create such an overview. The outcome is a structured database containing 4,296 company profiles across 64 countries. Below are some of the key trends identified.

This analysis relies on a structured dataset compiled from OEM partner directories, corporate websites, business registries, industry associations, screenings of major trade-show exhibitors, and analyst reviews. While coverage differs by country and online visibility, the structural trends are evident.

A vast ecosystem led by small enterprises

Among the approximately 3,400 companies with available employee data, 54% have fewer than 50 staff members. Only 5% employ over 1,000 people. The top 5% of firms by headcount represent 84% of total employment in the dataset—a classic long-tail distribution. The robotics ecosystem consists of a handful of large conglomerates and numerous specialized small firms.

Regionally, Europe accounts for 47% of all profiles, APAC for 29%, and the Americas for 23%. The top five countries—the United States (536), China (441), Germany (339), Japan (270), and France (248)—comprise 43% of the total.

China presents a unique scenario. The actual number of system integrators likely reaches into the thousands, but many smaller entities lack a web presence, and the market is rapidly consolidating. Our 441 Chinese profiles are drawn from over 14 years of project work in the country—the actual ecosystem is far more extensive than any structured database can fully represent.

A significant portion of the channel operates independently

ABB Robotics Unveils OmniVance Autonomous Surface Finishing Cell

ABB Robotics stated that this finishing cell aims to bridge the gap between custom automation and entry-level toolkits. | Source: ABB RoboticsABB Robotics recently introduced its first fully automated sanding and polishing cell. The Zurich-based comp

ABB Robotics Unveils OmniVance Autonomous Surface Finishing Cell

ABB Robotics stated that this finishing cell aims to bridge the gap between custom automation and entry-level toolkits. | Source: ABB RoboticsABB Robotics recently introduced its first fully automated sanding and polishing cell. The Zurich-based comp

FANUC America Announces $90 Million Investment in U.S. Robotics Manufacturing

FANUC is constructing a new facility to boost its robot manufacturing capacity in the United States. Source: FANUC AmericaAlthough the U.S. is a key robotics market, none of the top industrial automation companies are based there. This landscape is c

FANUC America Announces $90 Million Investment in U.S. Robotics Manufacturing

FANUC is constructing a new facility to boost its robot manufacturing capacity in the United States. Source: FANUC AmericaAlthough the U.S. is a key robotics market, none of the top industrial automation companies are based there. This landscape is c

AI Robotics Transitions from Lab to Factory Floor

From left: Andy Lonsberry of Path Robotics; Anders Beck of Universal Robots; and Dave Coleman of PickNik Robotics.Artificial intelligence is now a fundamental part of every robotic system. It transforms how robots interpret sensor data, make decision

AI Robotics Transitions from Lab to Factory Floor

From left: Andy Lonsberry of Path Robotics; Anders Beck of Universal Robots; and Dave Coleman of PickNik Robotics.Artificial intelligence is now a fundamental part of every robotic system. It transforms how robots interpret sensor data, make decision

2026 Latest Best AI Expense Trackers: Top-rated tools to scan receipts & categorize corporate spend automatically. Discover powerful, game-changing solutions for effortless expense management, accurate financial tracking, and streamlined compliance. Our curated, weekly-updated comparison of free vs paid options helps you find the perfect fit. Unlock your AI edge with XIX.AI's expert picks.

10 tools

xix.ai

Discover the 2026 latest top-rated AI recruiting tools on XIX.AI. Our curated list features powerful, game-changing solutions for screening resumes and automating candidate interview scheduling. Compare free vs paid options with real-world tests and weekly updated rankings. Find your perfect hiring assistant and streamline your recruitment today!

10 tools

xix.ai

Discover the 2026 best AI personal wellness and focus coaches on XIX.AI. Our curated rankings feature top-rated, game-changing tools to manage burnout and boost mental energy. Compare free vs paid options with real-world insights. Unlock your path to peak productivity and well-being today.

10 tools

xix.ai

Discover the 2026 latest top-rated AI romantic chatbots for building genuine, long-term connections. Our curated list features powerful, consistent personalities, free vs paid comparisons, and real-world tests. Find your perfect companion and start building today at XIX.AI.

10 tools

xix.ai

Discover the 2026 best AI data science mentors to master SQL, Pandas & ML workflows. Explore our top-rated, curated selection at XIX.AI for powerful, game-changing guidance. Compare free vs paid options with real-world insights. Unlock your data science mastery today.

10 tools

xix.ai

Discover the 2026 best AI flirting and conversation trainers on XIX.AI. Our curated, top-rated selection helps you build social charisma and confidence in real-time. Explore must-try, game-changing tools with free vs paid comparisons and weekly updated rankings. Unlock your social edge today.

10 tools

xix.ai